The Rise of the Non-Traditional Energy Buyer

John Powers leads the Renewable Energy Advisory Services Division at Renewable Choice Energy and has helped corporate and institutional clients achieve their renewable energy goals for over 12 years.

This is the first in a 4-part series of blogs on the explosive renewable growth currently underway in the commercial & industrial market sector.

A sea change happened in 2015 as the momentum of renewable energy reached and surpassed a tipping point that many of us in the industry had envisioned but never fully realized would happen.

Yet here we are. Rapid technological advancements, price parity, broad-based consumer and NGO support, and coal’s inevitable demise finds us at the frontier of a new electricity landscape about to be dominated by renewables.

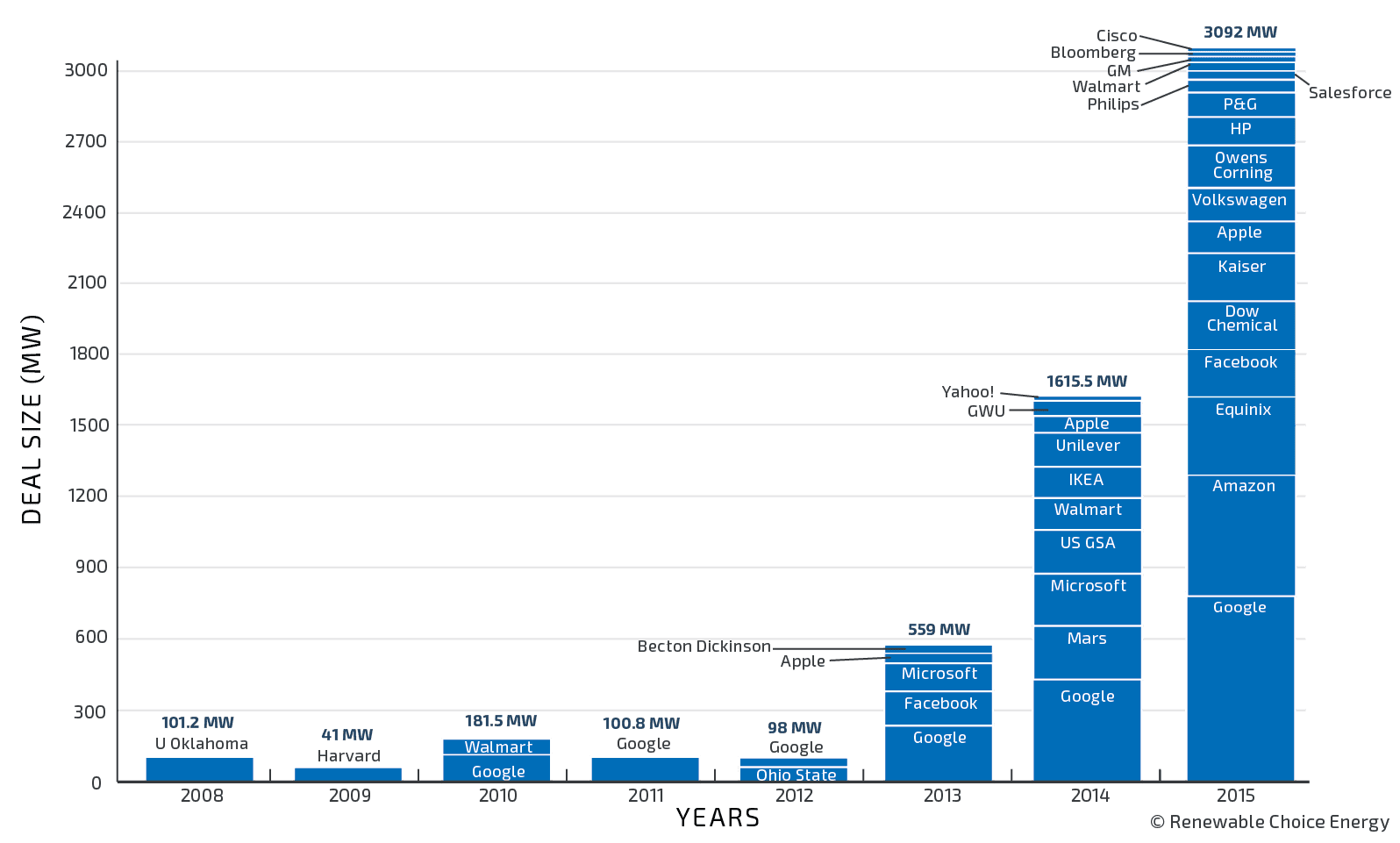

The renewable energy industry had a powerful ally in the last few years, and 2015 in particular: the corporation. As prices in wind and solar have fallen, support for these technologies in the commercial & industrial (C&I) sector has swelled. In 2015, C&I buyers invested in more than 3 gigawatts (GW) of new renewable energy capacity. Google alone purchased nearly a gigawatt of new wind and solar projects in 2015, making them the largest institutional buyer of renewable energy in the world.

Why are organizations suddenly so hungry for renewable energy? And, importantly, how can developers respond to this new customer class that differs from a traditional utility or bank buyer?

The corporate quest for clean energy is not entirely new, as most readers will recognize. Since Whole Foods Market announced their adoption of 100% wind power back in 2006, an increasing number of companies have followed suit. Renewable Energy Certificates (RECs) have gone from an obscure—and frequently questioned—mechanism for delivery of green power to the recognized industry standard, used by thousands of organizations by the billions of kilowatt hours every year.

Many companies have also pursued the development of onsite solar, and, in some cases, wind turbines and geothermal power, in order to meet at least a portion of their electricity demands. While this remains a viable partial solution in certain markets, the inherent challenges around size and resource availability make it difficult to meet large renewable energy or carbon reduction goals with onsite alone.

Several colluding factors are driving this new dogged pursuit of large volume, additional, clean energy:

- Ever increasing needs for electricity. It’s no surprise that data center companies have been the early adopters of corporate power purchase agreements (PPAs); the rapidly expanding appetite for data space in every sector means that organizational footprints are on the rise, too. This won’t change; back in 2013, the EIA projected that world energy consumption would increase 56% by 2040.

- Price volatility in traditional markets. Price swings in fossil fuel markets can translate into millions of dollars of additional energy costs for large companies, and, because of their fluctuating volatility, these are increases that are not always predictable, making it difficult for companies to accurately budget and plan for electricity expenses. Sourcing electricity from wind or solar via a PPA provides buyers with stability that supports both the setting and achieving of budgetary goals.

- Attractive cost incentives. The Production Tax Credit (PTC) and Investment Tax Credit (ITC) both provide lucrative incentives that can bring the price of new wind and solar below the projected market cost for traditional energy. For the C&I PPA buyer, this can translate into savings in the millions of dollars per project over what the organization might have spent on fossil fuel-based electricity. A falling price environment makes PPAs extremely attractive to large-scale buyers.

- Broad-based support—and pressure—for companies to set and achieve emission reduction targets. Thanks to the efforts of organizations ranging from CDP to Greenpeace, American corporations are under a tremendous amount of pressure to report on and reduce their carbon footprint. Last year, hundreds of companies made public commitments—ranging from joining the RE100 to signing the White House’s American Business Act on Climate Pledge—to reduce carbon emissions, act on climate change, or secure renewable energy. In order to fulfill those goals, C&I buyers are looking for solutions, like PPAs, that allow them to purchase large volumes of renewables over long periods of time.

While C&I buyers are hungry for the renewable energy opportunity, they also face hurdles to acquisition that are atypical in a utility environment. Unlike banks and utilities, who are themselves the source of credit, C&I buyers must establish their creditworthiness if they are to be considered a serious off-taker. There is also a need for organizations to engage multi-departmental stakeholders ranging from the treasury to accounting to the legal department; in some cases, deals can fall through because of one individual’s objection.

C&I buyers are generally unfamiliar with the risk profile presented in a long-term PPA, as power purchasing is typically done on the spot market or in 1-to-3 year strips. Getting them comfortable with things like forward market price projections or the basis risk between the wind farm and their load can be a big lift. Deals can take a long time to coalesce because of the need for organizations to complete thorough due diligence.

While all these barriers can be overcome, for developers, working directly with a corporate or institutional off-taker represents a new challenge. Education becomes a key component of the transaction; identifying and eliminating risks is paramount. C&I customers want to know if the project they are seeing is really the best project in the market and if the terms they are being presented are fair. Decision-making cycles for a new transaction of this type and a Fortune 500 company can be quite long, as there are many departments involved and the ultimate signatories are nearly always executive-level.

For these reasons, many developers are choosing to work with buyer’s agents. A respectable buyer’s agent will fully vet both parties prior to making recommendations to ensure the highest likelihood of success. The buyer’s agent will also deeply understand the buyer’s goals and objectives, and can help communicate those to a developer, allowing the developer to more closely tailor the PPA to the buyer. It is rare that companies can get PPA deals done on their own, especially the first time; working with a buyer’s agent can save time and money upfront.

If 2015 gives any indication, we’ve only begun to see the rise of the non-traditional energy buyer. Developers who hope to partner with these companies can help themselves achieve success by learning more about this emerging customer class and how to speak their language.

Renewable Choice is the leading supplier of renewable energy solutions to commercial, higher education, and municipal clients in North America, acting as a buyer’s agent on over 1 GW of long-term PPAs and supplying millions of MWh of RECs. The company is the 2012, 2014, and 2015 EPA Green Power Supplier of the Year. Learn more at www.renewablechoice.com.